A project to build two energy islands in Denmark, the largest construction project in Danish history to date, have been greenlit by the Danish government, one in the North Sea, and in the Baltic Sea. Of course this also means that there are important considerations to make in order to successfully navigate compliance and taxation in energy constructions.

This marks a significant milestone in the Denmark’s infrastructure. These energy islands are not just marvels of engineering, but also significant players in the landscape of compliance and taxation, especially for employers involved in their construction.

Read more about the Danish energy islands in general, the introduced taxation in brief, or the taxation of individuals.

A project to build two energy islands in Denmark, the largest construction project in Danish history to date, have been greenlit by the Danish government, one in the North Sea, and in the Baltic Sea. Read more about the Danish energy islands in general, the introduced taxation in brief, or the taxation of individuals.

Navigating compliance and taxation in energy construction

As a company engaging in activities within Denmark’s expanded exclusive economic zone, it’s crucial to anticipate the likely creation of a permanent establishment in Denmark. This would entail taxation on corporate income and necessitate meticulous adherence to reporting and withholding rules for employees stationed at these energy island locations.

Taxation norms for individuals, barring those involved in labour outsourcing, will adhere to standard progressive taxation. Each employee will be required to register for a preliminary tax assessment. This will provide the necessary information for the employer (the permanent establishment) to perform accurate tax withholding and payments.

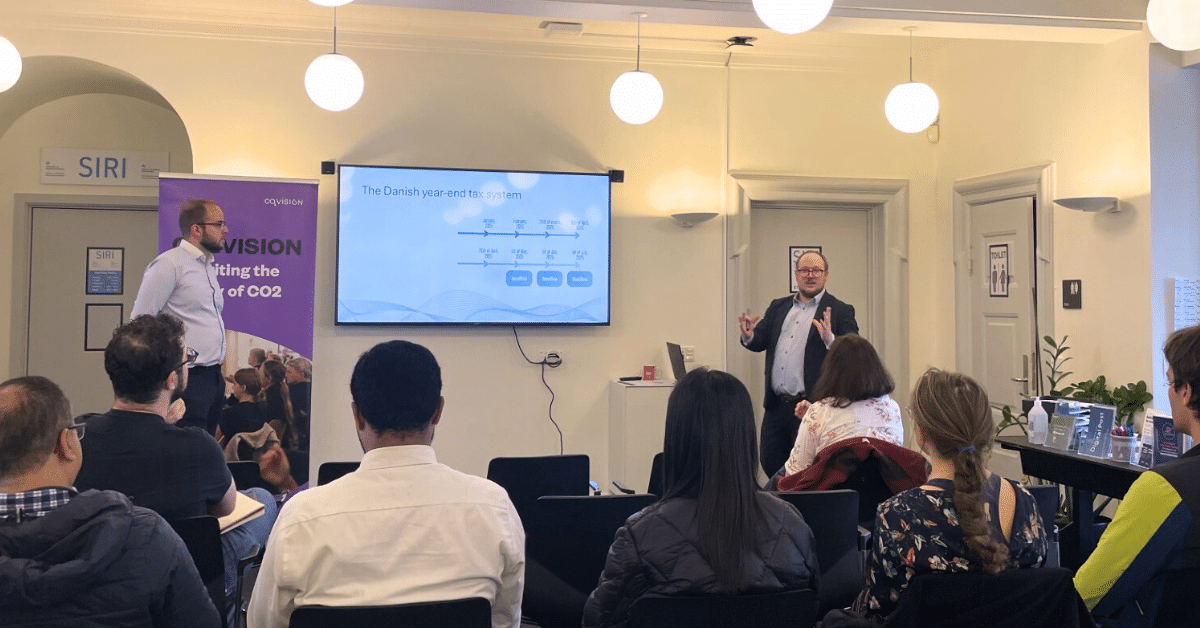

At the end of the fiscal year, the Danish tax authorities will generate a year-end statement for each individual, typically available in early March. This comprehensive document will facilitate clarity and transparency in taxation matters.

In conclusion, the dawn of the energy islands era in Denmark ushers in a unique set of compliance and taxation challenges. Businesses and individuals associated with these projects must be equipped with an in-depth understanding of the evolving tax landscape to navigate this new reality successfully.

Compliance and taxation

As an employer working on any installation in Denmark’s exclusive economic zone, you should prepare for the highly likely scenario that there will be a permanent establishment in Denmark. This will mean that the corporate income will be taxable and that reporting and withholding should be observed for the employees that will work in Denmark on these locations.

With the exception of hiring-out labour the taxation for individuals will be the ordinary, progressive taxation. Each employee must register with a preliminary tax assessment in order to generate the details for the employer (the Permanent establishment) to perform correct withholding and tax payment.

By year-end the individual will have a year-end statement produced from the Danish tax authorities (typically available early March).