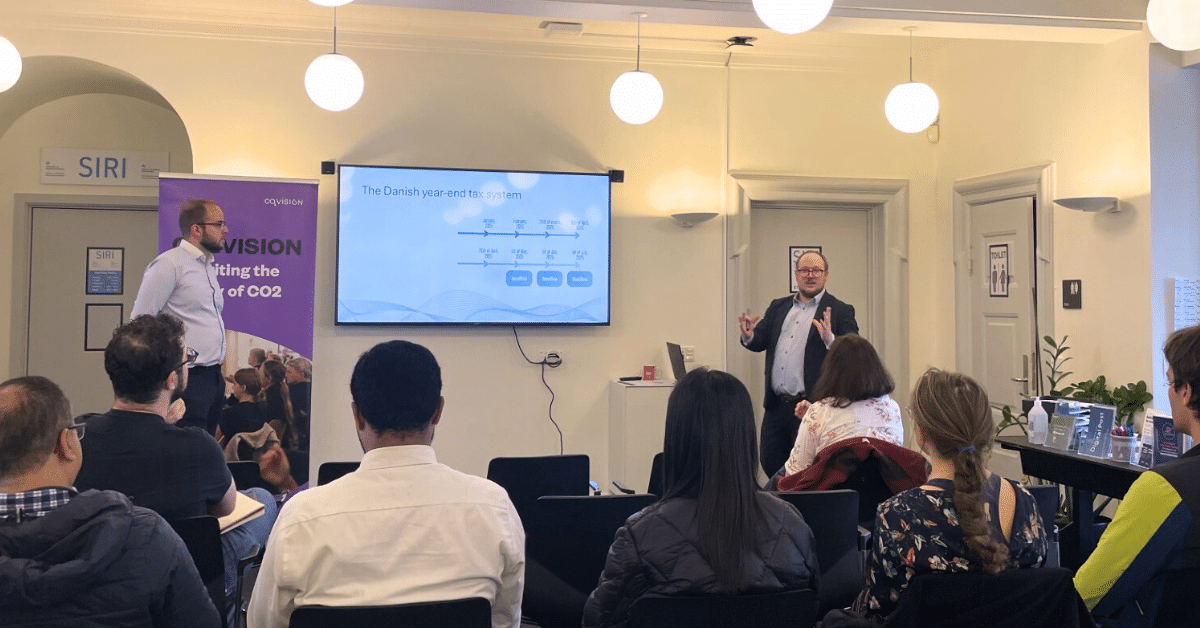

The Danish year end tax statement can be quite confusing even to Danes, so while it is now availble in English for foreigner, it can still be a cause for confusion, especially for individuals with international elements, e.g. individuals who have residence, income, or assets abroad, who have relocated to or from Denmark during the tax year, or if certain tax schemes apply, such as the frontier worker or the tax scheme for researchers.

The year-end statement (årsopgørelse) is now available in English, making it easier for non-Danish speakers to review and correct their tax information. However, certain elements-such as foreign income, property, or investments-still require manual reporting and are easily overlooked.

In Denmark, timely and accurate tax reporting is essential for both individuals and businesses, with the primary deadline for submitting tax information set for January 20th of the year following the income year, and a correction period until February 15th to ensure all data is accurate and up-to-date.